Usually when looking for trades, one starts with the longer time-frames and works ones way down to the shorter time-frames and since my English teacher once warned me that using the term 'one' traps one in a paradoxical situation where one can no longer use any other term other than 'one', I will be switching to 'you'. So, when you are looking for a trade, you normally start with the longer term time-frames and work your way down to the shorter term time-frames. This allows you to find the good strong weekly trending shares, then down to the daily for confirmation and then onto the 1 hour picture to try and optimise entries and exists.

In this case though, we are already in the BIL trade, I will start with the smaller time-frame and work my way up. Now before going any further, you must understand the nature of this particular trade. This is exactly what the name suggests, a trade, not a long term investment but a short term trade aimed at making a percent to add to the kitty.

Ok then, first up is the 1 hour picture. Here I have indicated a few things:

1.) The entry trigger - Trend line that was broken

2.) The target for the trade - A recent high

3.) A bearish signal - A Shooting Star candle formation (the reason for thinking about the trailing Stop-Loss)

4.) The trailing stop-loss - trend line that if broken, will trigger an exit out of the trade

|

| BIL - 1 hour |

Perhaps getting out when that trailing stop-loss is triggered will be too soon as we know that nothing moves up (or down) in a straight line. None the less, we can always buy it back and aim for the R307.50 target after it has retraced a little.

Moving on to the Daily picture, a few things stand out:

1.) The trend has changed to Bullish - Indicated by the circle as there is a convergence of moving averages as well as a price move above that all important 89 moving average

2.) The long trigger line is made a little more clear

3.) The price is moving up from an oversold position - Bodes well for a bullish move

4.) Longer term Fibonacci price target - Target is R320.00 and since this is Fibonacci

* There is also bullish divergence here, but I think that someone should point it out in the comments, or mail a chart that shows the divergence to me (petri@rockcapital.co.za) and I will then put in on the blog as part of this write up. Only one way to get interaction from your readers and that's to make them work a little ;)

|

| BIL - Daily |

So that there is a much bigger target on the daily picture than there is on the 1 hour picture, you might find yourself asking why we are not targeting R320.00 but rather R307.50 and the answer is rather simple. Well maybe not that simple, but simply put, the strategies used for shorter term time-frames and longer term time-frames are different. This is too much to get into now, so I will leave it at that for the time being.

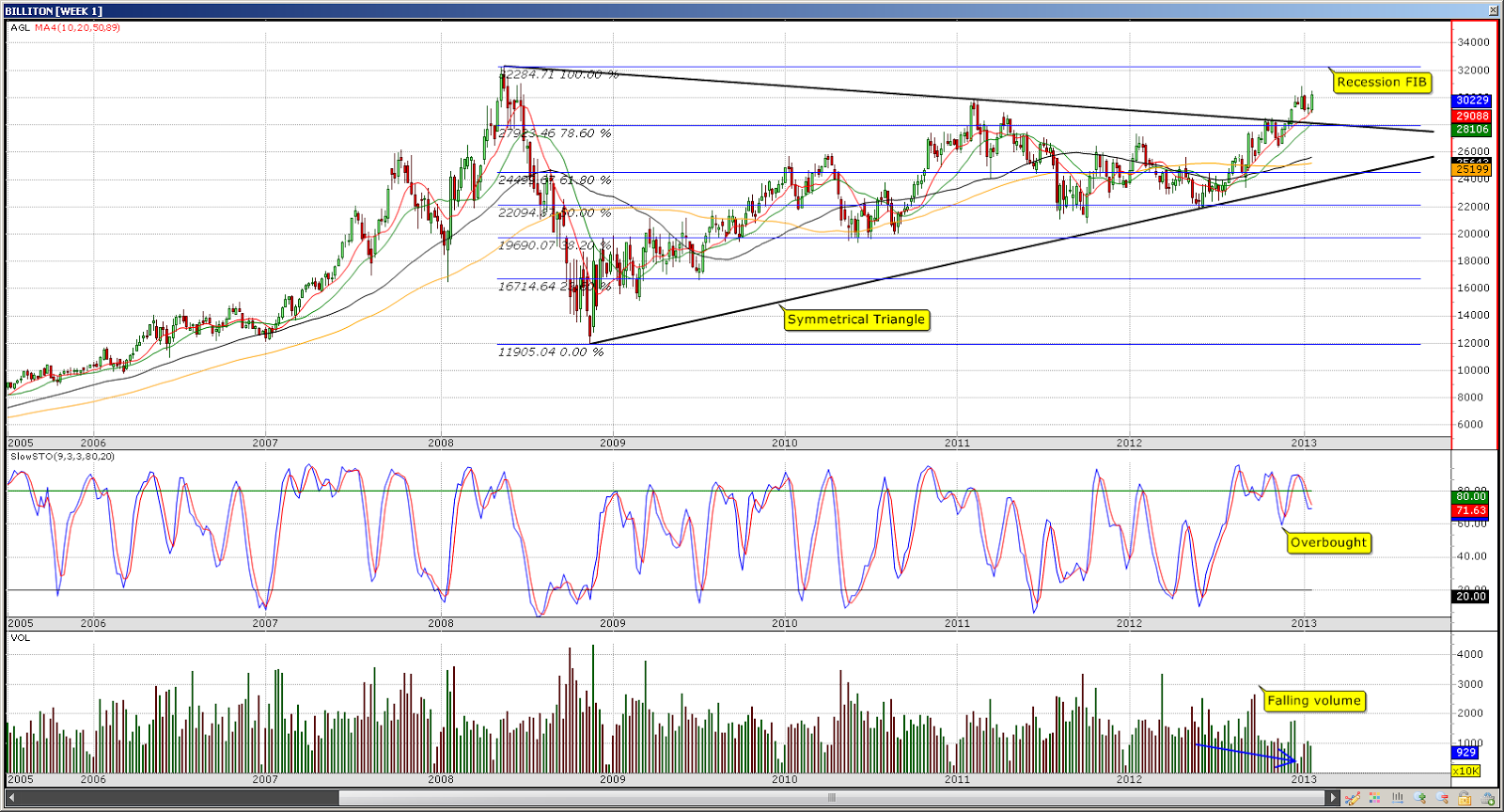

Again, moving onto a higher, or longer, time-frame - the weekly. Here we see a few things happening all at once:

1.) There is a very large symmetrical triangle with a very large target - it's very far away and will probably take years, but hey, inflation is on our side and it will probably reach there at some point

2.) Recession Fib showing key support and resistance levels - see how that Fibonacci target on the daily almost lines up with the high's of old?

3.) It looks slightly overbought and the volumes are starting to fade a little - this could indicate that it is going to come back to test that triangle break out before moving further up, although note that this is a weekly chart and that re-test can take weeks or months to play out, just like reaching the target for that triangle can take years

*In general though, it does look pretty bullish.

|

| BIL - Weekly |

And that in a nutshell is a, although done backwards, technical view on BHP Billiton PLC. Please leave your questions and comments below and we will be happy to respond to them. Also don't forget that if you spot the Bullish Divergence on the Daily Chart, email me at petri@rockcapital.co.za and I will put in here.